EIEIO...Progress, Not Perfect

“For those that don’t know history…everything is unprecedented.” – Condoleezza Rice

“The precautionary principle - better safe than sorry - condemns itself: in a sorry world there is no safety to be found in standing still.” – Matt Ridley

“Success is not final, failure is not fatal. It is the courage to continue that counts.” – Winston Churchill

What a mess.

A global pandemic resulting in millions of deaths and disruption. Bank runs. Racial tensions. Catastrophic war. Geopolitical fragility.

While these could be headlines today, these were the same problems we had 100 years ago.

In the early 1920s, the Spanish Flu pandemic had raged for over two years, killing 50 million people globally (versus 6.8 million for COVID) and 675,000 Americans. WWI had just come to a close with a death toll of 22 million (the cost of US involvement in the war was over 50% of total American GNP).

Moreover, Americans were only a few years into a decade-long banking crisis. 600 banks failed per year from 1921 and 1929. Racial violence was omnipresent. KKK nationwide membership had ballooned to 2 million people and led to atrocities like the Tulsa Massacre in 1921 (injuring 800+ people and killing up to 300).

If you were a young high school graduate 100 years ago, it would be understandable if you thought you got dealt a bad hand. And perhaps thinking that the only good news was that it couldn't get any worse, 1929 was the beginning of the Great Depression. The following decades brought the Dust Bowl, WWII, the Korean War, the Cold War, and continued racial turmoil – to name just a few of the 20th century’s greatest hits.

Even with all these crushing problems American society has faced, life has moved up and to the right for the country. GDP per capita has gone from $6,460 to $76,658, life expectancy for a male has gone from 53 to 76, and the Dow Jones Industrial Average has gone from $90 to $33,000 (36,566%), just to name a few facts.

It’s ironic how anxious many young people are today who dread the future often yearn for “the good old days'' given this reality. Selective nostalgia is counterproductive. Though the past century was plagued by crises, conflicts, and disasters (just like every other era in human history), the progress that was made during the same timeframe was utterly world changing. People have gotten healthier, wealthier, and wiser at an incredible rate, and our continued positive trajectory as we head into the Brave New World is cause for optimism.

Healthy: It was not long ago that strep throat was usually fatal, ear infections commonly developed into chronic conditions, and the only treatment for tuberculosis was “fresh air”.

From 1915 to 1997, infant mortality dropped by 96%

From 1913 to 2013, average global life expectancy went from 34 to 71 years

Since its first use as a medicine in 1942, it’s estimated that Alexander Fleming’s discovery of penicillin has saved over 200 million lives

Patients at an outdoor “Tuberculosis Colony” in pre-antibiotics, 1920s England

Wealthy: From author Matt Ridley’s The Rational Optimist – In 2010, of Americans officially designated as ‘poor’, 99% had electricity, running water, flush toilets, and a refrigerator; 95% had a television, 88% a phone, 71% a car, and 70% air conditioning. Cornelius Vanderbilt had none of these.

In 1910, 74% of the world was living in extreme poverty. In 2015, that number had plummeted to 10%.

In 1920, the United States barely had a middle class. In 2021, 50% of American adults live in middle class households.

In 1920, about 10% of American households owned stock. Today, nearly 60% own stock.

Wise:

In 1920, just 17% of Americans graduated from high school and a mere 5% graduated from college. By 2019, those numbers had risen to 86% and 38%, respectively.

Due to advances in structural engineering and improvements to emergency response, there has been a 92% decline in the decadal death toll from natural disasters since its peak in the 1920s. In that decade, 5.4 million people died from natural disasters. In the 2010s, 400,000 did. During that same period, the global population nearly quadrupled.

The transition from a manufacturing-based economy to a knowledge-based economy caused workplace injuries and deaths to plummet. In 1907, Allegheny County, Pennsylvania (population 1 million) experienced 526 deaths from “workplace accidents.” In 2019, the number of workplace fatalities for the entire state of Pennsylvania (population 12.8 million) was 154.

Shifting from nuts & bolts to bits & bytes made Americans far safer

It hasn’t been perfect, but we’ve seen much more progress than pain over the last 100 years. We’re entering a Brave New World, and the most important currency won’t be money – it will be time. Ben Franklin wrote that “Time is Money” in 1748…the same is true today.

While the concept of “Time is Money” has been around for a while, what’s changed is the agency in how we choose to allocate our time. The 1900s was a century that shifted peoples’ focus from surviving to thriving; with each new technological breakthrough, more people were able to focus on the next new challenge.

New breakthroughs are allowing peoples’ payback on time to dramatically increase. We’re already seeing this with knowledge workers and LLMs – 1 in 5 Americans can do their job at least 50% faster thanks to AI.

While we’re just as excited about ChatGPT as the next person, the massive impact of this time dividend will also be in the world of atoms, not just bits.

Let’s start with travel in the United Arab Emirates. At the Dubai Airport, travelers’ eyes become their passports. This doesn’t just get you through security quicker…it lets the person who used to stamp passports do something that’s more human. Anything a computer can do better, cheaper, and faster than a human, it should do (as an aside, going from Dubai to the Delhi Airport Passport Control was like going from the Jetsons to the Flintstones).

This year, Dubai will have self-driving taxis. Anybody who’s been in a taxi flying up and down Sheikh Zayed Road knows that in the worst case, an autonomous taxi couldn’t be any more dangerous than the human version. It’s estimated that autonomous vehicles will reduce auto deaths by over 90%. Moreover, autonomous vehicles will unlock a significant productivity boost. Americans currently spend an average of nearly 300 hours (or 7.5 work weeks) per year behind the wheel.

Dubai, which has become the Window to the Future (and by the way, recently opened up the Museum of the Future), will by 2026 have flying taxis.

And by 2030, Boom Overture will introduce supersonic jets that fly twice as fast as standard jets. Initially, this means being able to go from Dubai to Singapore in 4 hours. The company’s long-term mission is to get anywhere in the world in four hours for $100.

The United Arab Emirates isn’t just following the path to the future; they’re building it. As Marc Andreessen puts it,

“Our nation and our civilization were built on production, on building. Our forefathers and foremothers built roads and trains, farms and factories, then the computer, the microchip, the smartphone, and uncounted thousands of other things that we now take for granted, that are all around us, that define our lives and provide for our well-being. There is only one way to honor their legacy and to create the future we want for our own children and grandchildren, and that’s to build.”

Technology creates time…the question is how people will spend it. In 1930, John Maynard Keynes famously wrote an essay titled “Economic Possibilities For Our Grandchildren."

In the essay, he predicted that by the time his children had grown up, people might be working just 15 hours a week. And while Keynes got some things right, this particular prediction was a Freezing Cold Take.

There’s a lot of reasons why, but the most important one is that people want to make the most of their time on Earth – and that includes their job. A McKinsey study found that 70% of people across industries define their purpose through their work.

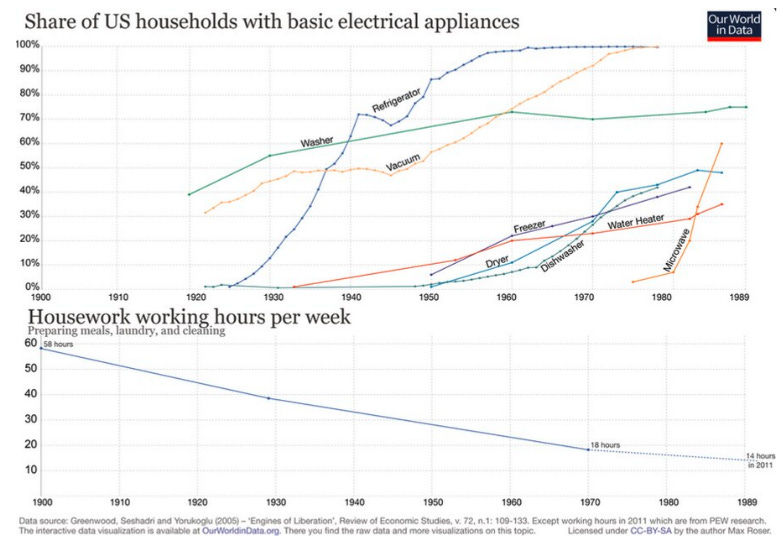

More innovations has meant more time, and more time has meant better outcomes. Take chores for example. More electrical appliances, fewer hours spent doing housework per family per week. These inventions also gave way to a major rise in female workforce participation in the United States.

By focusing on what people are put on Earth to do and taking advantage of how technology can do things that are fungible, the possibilities become open-ended and wildly exciting for our future.

Technology will give us more free time, and people have to choose whether to spend their “time dividend” endlessly pursuing different forms of R&R or trying to make a difference in the World. We need more people to choose the former if we want to attack and solve the World’s Hardest Problems in the next 100 years with the same vigor as we did in the past 100.

We already got a sneak peak of this dilemma during the COVID lockdown. The most disciplined people got focused and started businesses while others filled their time in quarantine compulsively online shopping. As Lou Holtz says, “you get better, you get worse. You don’t stay the same.”

In some ways, COVID was a precursor of things to come. to the future of a world where we’ll all have more time to focus on what we truly care about. Flying taxis and faster writing won’t just make our lives easier…they’ll make them more meaningful. As Linda Ellis puts it in “The Dash”:

For it matters not, how much we own,

The cars...the house...the cash.

What matters is how we live and love

And how we spend our dash.

Our belief isn’t that people should have a fulfilling life working 12 hours a day in a coal mine. It’s clearly the opposite. But working and feeling like what you’re doing matters is an important part of the living experience. It’s not man versus machine; it’s man and machine.

Make your dash count!

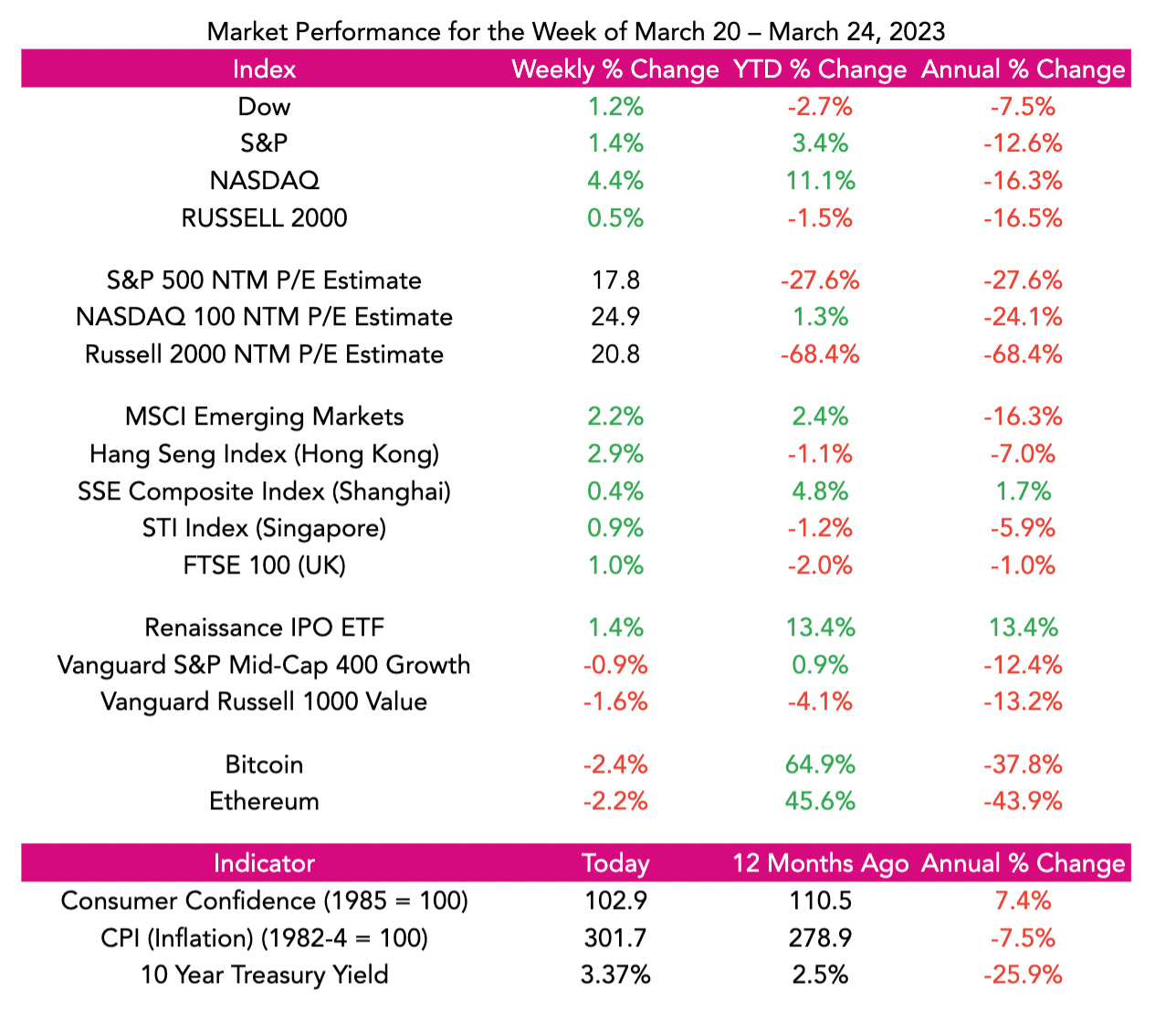

Market Performance

In a week where the countries who are the two largest threats to the United States were all lovey-dovey in Moscow, and Iran bombed U.S. contractors in Syria, mortal enemies Saudi Arabia and Iran decided they should be friends at the urging of China…the news people seemed to care about was whether former President Trump would get indicted or not.

Even with all the geopolitical land mines going off, and the Fed raising rates 25 basis points, the Market chugged ahead with the Dow up 1.2%, the S & P 500 advancing 1.4% and NASDAQ increasing 1.7%.

While there are many things to worry about, and there are always many things to worry about…and all the strategist are negative….the fact that stocks are holding up suggest to me that there is opportunity on the upside and focusing on companies that have the best growth prospects with the 5P’s (people, product, potential, predictability and purpose) should do well.

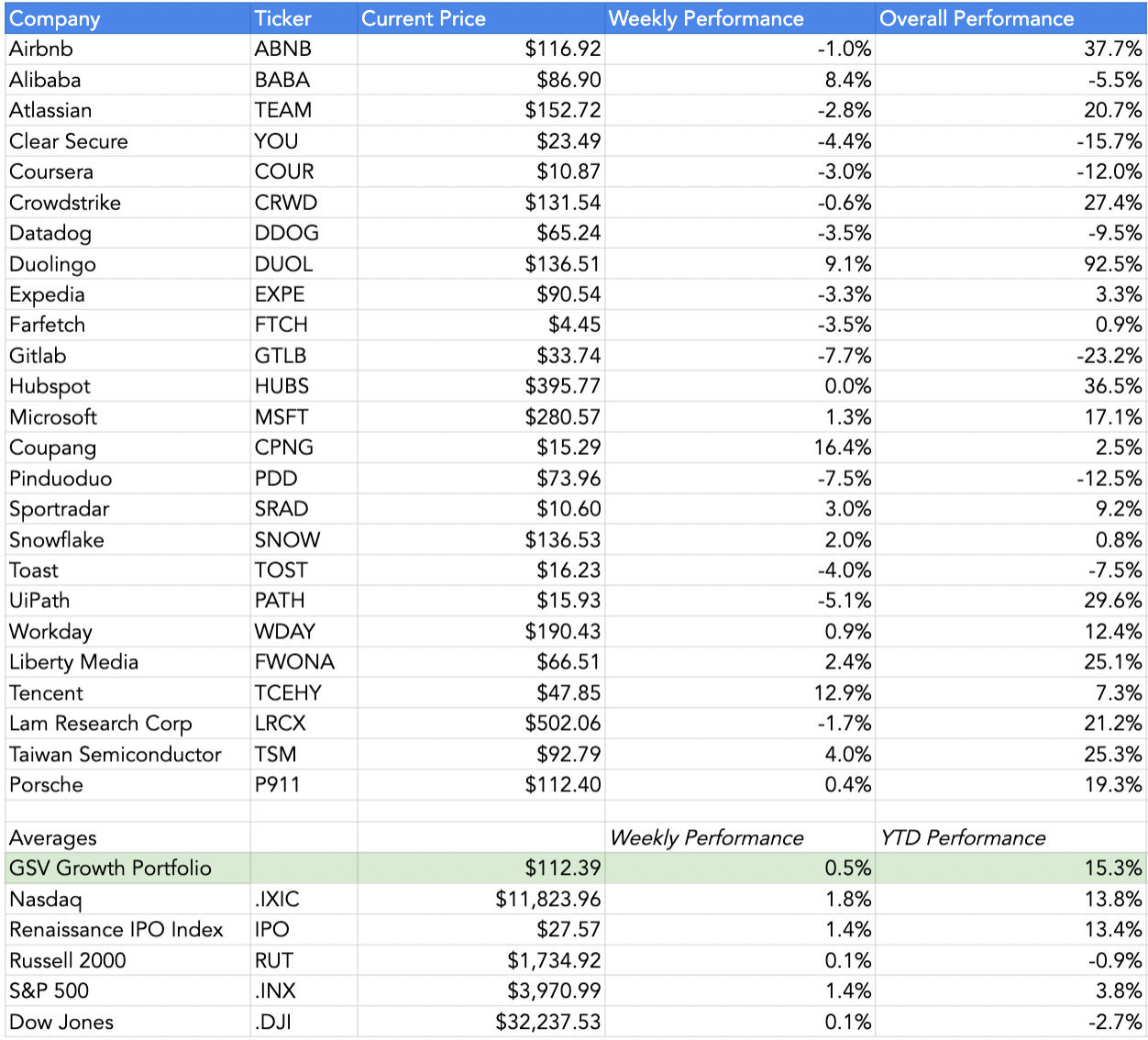

GSV’s Four I’s of Investor Sentiment

GSV tracks four primary indicators of investor sentiment: inflows and outflows of mutual funds and ETFs, IPO activity, interest rates, and inflation. Here’s how these four signals performed last week:

#1: Inflows and Outflows for Mutual Funds & ETFs

Source: Yardeni

#2: IPO Market

The US IPO market remains quiet. However, three international companies made headlines this week: Rappi, Renault’s EV Unit, and Rakuten Bank. Rakuten Bank would be the largest IPO in Japan since 2018.

Source: Renaissance Capital

#3: Interest Rates

Despite the recent banking turmoil, the Fed hiked rates by 25 basis points this week.

#4: Inflation

Inflation continues to ease, but it’s still a long way from the Fed’s 2% annual inflation target.

Source: Investopedia

Videos of the Week

Chart of the Week

Chuckles of the Week

Picture of the Week

UBS Chairman Colm Kelleher looks like he just swallowed a $%&* Sandiwch.

EIEIO…Fast Facts

Entrepreneurship: 59% — percent of Founders that think the fall of SVB is going to make the startup fundraising environment tougher (Source)

Innovation: 150 million — number of Americans on TikTok, up 50 million since 2020 (Source)

Education: 12:00 AM - 1:00 AM – most popular time to take classes on edX around the world (Source)

Impact: 72% –percent of Americans who are living paycheck-to-paycheck that could benefit from early-wage access (Source)

Opportunity: 55% – percent of heterosexual couples that meet online, up from 37% in 2017 (Source)

Connecting the Dots & EIEIO…

Old MacDonald had a farm, EIEIO. New MacDonald has a Startup…. EIEIO: Entrepreneurship, Innovation, Education, Impact and Opportunity. Accordingly, we focus on these key areas of the future.

One of the core goals of GSV is to connect the dots around EIEIO and provide perspective on where things are going and why. If you like this, please forward to your friends. Onward!

Make Your Dash Count!

-MM